Economy Faces 'Shutdown', This Asset Has 50% Upside

Bulls roar while storm clouds gather

TABLE OF CONTENTS

100% Tariffs: The U.S.–China Showdown That Could Shake the World

Trader Reveals ‘Bubble’ Assets; How Does Market Mania End?

Major Crash Starting For Gold, Silver? What’s Next After Biggest Drop In Months

Economic Boom Or Crash Next? Turning Point Reached

Start Of Monetary Reset? What’s Next For Bitcoin, Gold, Dollar

Interest Rates To Zero, Rents Will Double; Grant Cardone On ‘Explosion’ In 2026

Biggest Silver Squeeze Ever: Is $100 Next Or Collapse?

Market Recap

United States equity markets demonstrated resilience through a week marked by strong corporate earnings and improving trade sentiment, though volatility returned midweek as investors digested mixed results from technology leaders. The S&P 500 opened the week with a robust 1.2% advance on Monday, October 20, reaching 6,664, while the Dow Jones Industrial Average climbed 1.1% and the technology-heavy Nasdaq Composite led with strong gains. Tuesday brought record-setting performance for the Dow, which rose 218 points to close at 46,924.74, briefly surpassing 47,000 intraday, while the S&P 500 closed just above the flatline at 6,735.35. Wednesday witnessed a reversal as markets pulled back on disappointing Netflix earnings, before recovering Thursday with the S&P 500 rising 0.58% to close at 6,738.44 and the Nasdaq Composite outperforming with a 0.89% advance to settle at 22,941.80. Friday’s trading brought fresh momentum as the September Consumer Price Index report showed inflation rose 3.0% annually, below the expected 3.1%, with monthly gains of 0.3% against forecasts of 0.4%, strengthening expectations for another Federal Reserve interest rate cut at next week’s policy meeting. Trade relations remained a focal point as the White House confirmed that President Trump will meet with Chinese President Xi Jinping on October 30 in South Korea ahead of the Asia-Pacific Economic Cooperation summit, while Treasury Secretary Scott Bessent stated that the United States and China had “substantially de-escalated” after recent trade tensions.

The third-quarter earnings season delivered several standout performances. General Motors reported spectacular results Tuesday, with adjusted earnings per share of $2.80, beating expectations of $2.31, and raised its full-year guidance significantly, with adjusted earnings before interest and taxes now projected at $12 billion to $13 billion, up from $10 billion to $12.5 billion. The Detroit automaker also reduced its expected tariff impact to $3.5 billion to $4.5 billion and surged more than 15% on Tuesday, marking its second-best day since emerging from bankruptcy in 2009. Traditional stalwarts Coca-Cola and 3M exceeded Wall Street estimates, jumping 4.1% and 7.7%, respectively. At the same time, Netflix delivered disappointing results after Tuesday’s close, missing earnings expectations and sending the stock down by over 10%. Intel Corporation reported Thursday after the close, beating expectations with revenue of $13.7 billion against forecasts of $13.15 billion and adjusted earnings per share of $0.23 versus projections of $0.01, sending the stock up over 8% in after-hours trading. Ford Motor reported Thursday with adjusted earnings of $0.45 per share, exceeding the $0.36 consensus, and record quarterly revenue of $50.5 billion. However, the automaker lowered its full-year guidance, citing an expected $1.5 billion to $2 billion impact from a September fire at aluminum supplier Novelis.

Market Movements

The following assets experienced dramatic swings in price this past week. Data are up-to-date as of Oct 24 at approximately 4pm EST.

(Data from StockAnalysis.com)

Shopify - up 9.63%

IBM - up 9.31%

CrowdStrike - up 8.80%

Netflix - down 8.73%

T-Mobile - down 5.04%

Oracle - down 2.74%

(Data from https://www.marketwatch.com)

DXY - up .27%

Bitcoin - up 1.78%

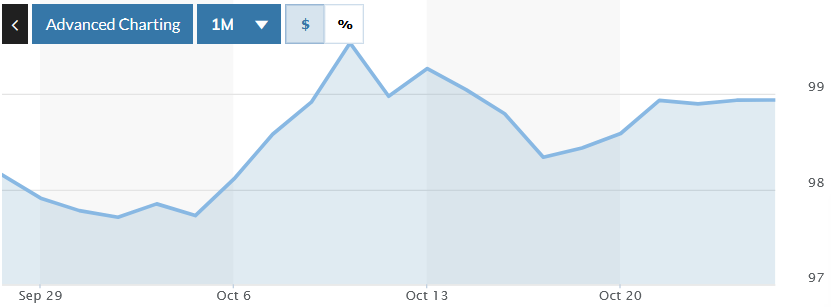

Gold - down 3.45%

Platinum - down 2.14%

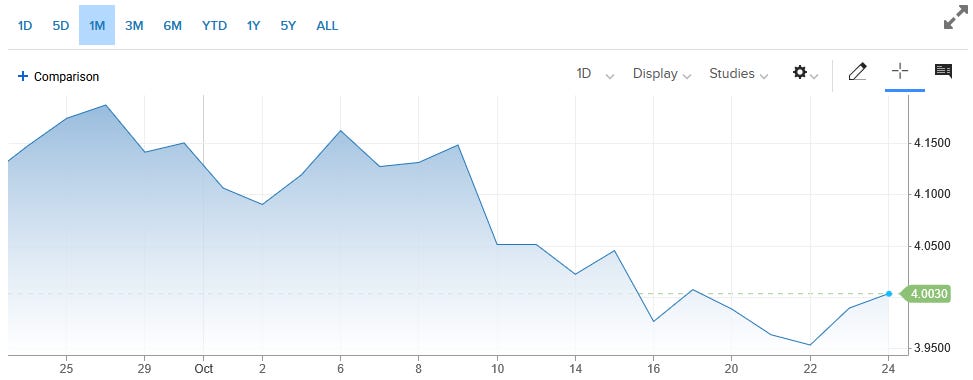

10-year Treasury Yield - down 2.00%

(10-year data from https://www.cnbc.com)

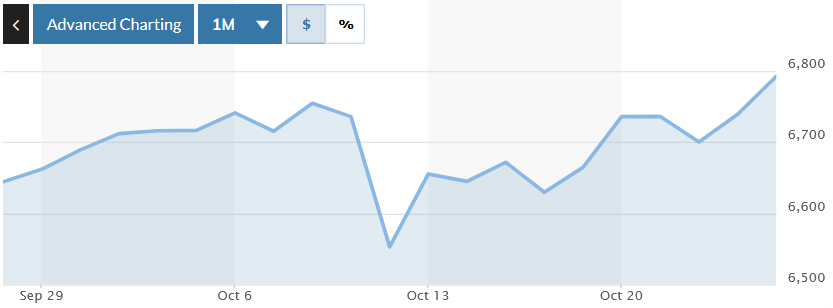

S&P 500 - up 1.50%

Russell 2000 - up 1.68%

Market Analysis

Steve Hanke, Professor of Applied Economics at Johns Hopkins University, returned to discuss his bold $6,000 gold prediction. Since his September interview, gold surged from $3,600 to $4,300. Hanke explained his forecast using historical patterns. “Gold is around 10% of the value of disposable personal income per capita in the United States” at secular bull market peaks, he said. The calculation had nothing to do with monetary policy or geopolitical events. The professor painted a grim picture of global uncertainty. He called European leaders “the three stooges” and said Germany pays triple the price for American LNG compared to its former Russian gas supplies. On China, Hanke said the country “could shut down the Western world in about six to nine months.”

Regarding Trump’s recently announced tariffs, Hanke rejected White House claims about who bears the cost. “Foreigners don’t pay for tariffs placed on foreigners. Americans pay the tariff,” he explained. He noted import prices rose at double the rate of other goods. Regional banks showed stress. Zion’s Bank fell 13% and Western Alliance dropped 10% after the banks disclosed bad loans. Hanke said rising delinquencies had been visible in aggregate data, but specific bank troubles focused investor attention. The economist predicted Federal Reserve rate cuts based on Chicago Mercantile Exchange pricing, with a 97% probability in October.

100% Tariffs: The U.S.–China Showdown That Could Shake the World

Shaun Rein, Founder and Managing Director of China Market Research Group, challenged Treasury Secretary Scott Bessent’s claims that the United States held leverage over China in the trade war. Bessent described the conflict as “China versus the world” and suggested that America possessed tools more powerful than rare-earth restrictions. Rein disagreed. “If China doesn’t export rare earths to the US, nothing in America works,” he said from Shanghai. China replaced American imports with alternatives. Beijing bought beef from Australia, soybeans from Brazil, and oil from Canada rather than from the United States. “Scotty Bessent is either fooling himself or he’s lying to the American people that they have more cards to play,” Rein explained. Trump’s 100% tariff announcement in October broke a detente established during Madrid negotiations between trade officials. The move prompted China to impose rare-earth export restrictions.

Chinese consumer spending remained depressed despite stimulus efforts. Weakness in real estate and stagnant wages dampened household consumption. “Nobody’s giving salary increases. No one’s giving bonuses right now,” Rein said. He suggested that the United States allow Chinese companies like BYD to build manufacturing plants domestically, similar to Toyota’s historical arrangements. National security concerns blocked such deals. Chinese students increasingly avoided American universities due to visa fears and costs reaching $400,000. “What’s the point of spending $400,000 US in America to go to a top private school?” Rein said. Starting salaries in China have fallen by 30% to 50% since the trade war began, making expensive foreign degrees economically irrational.

Trader Reveals ‘Bubble’ Assets; How Does Market Mania End?

Jason Shapiro, founder of the Crowded Market Report, questioned the usefulness of bubble talk in October markets. When asked about AI valuations, he pushed back on the concept itself. “The best definition I’ve heard of for bubble is a bull market that you’re not long,” he said. Shapiro noted concentration risks in the S&P 500, where tech stocks accounted for 44% of the index, and Nvidia alone accounted for 26%. He acknowledged that warning signs existed. “Companies like Oakllo, no revenues, and the stock’s up whatever 800% this year,” he said. Yet he refused to call market tops definitive.

On precious metals, Shapiro heard anecdotal evidence of retail interest. Friends asked about silver at Costco and mining stocks. “That’s the kind of things that certainly we know happens at a market top, but until they get all their money in, it’s probably not going to top,” he explained. Shapiro flattened his positions because markets began responding negatively to both good and bad news. For long-term investors, he recommended power generation stocks. “The power supply is the place that you would want to be invested,” he said, arguing that AI development required solving energy infrastructure regardless of whether technology delivered on promises.

Major Crash Starting For Gold, Silver? What’s Next After Biggest Drop In Months

Lobo Tiggre, Founder of The Independent Speculator, urged precious metals investors to take profits despite record rallies. Silver dropped 6.5% intraday before finding support at $50. Gold traded above $4,000, and miners showed triple-digit gains for the year. “Nobody goes broke taking profits,” Tiggre said repeatedly, defending his cautious stance against social media criticism. He described his “upside maximizer” strategy, a ratcheting stop-loss system designed to lock in gains. Tiggre noted retail interest reached a fever pitch. Silver sold out at Costco, and casual acquaintances asked about metals at dinner parties. “How bad would it be to be right, but not make any money?” he said.

Tiggre compared current conditions to 2011 when gold hit $1,911 intraday. Back then, mining stocks led metals lower for months as smart money exited. “The stocks led the way down in 2011,” he explained. This pattern had not emerged yet. The GDX mining ETF remained up 125% year-to-date despite a 9% single-day drop. Tiggre found the behavior encouraging. Stocks typically offer three to five times leverage to underlying metal moves. The modest decline suggested smart money had not fled. “I’d hate for them to wait for years, be right, but not make money or not keep the money they made,” he said of long-suffering gold bulls.

Economic Boom Or Crash Next? Turning Point Reached

Anna Wong, Chief U.S. Economist of Bloomberg Economics, turned bullish after years of bearish forecasts. She argued that a recession had already occurred in 2024 but went unnoticed due to overstated employment data. The Bureau of Labor Statistics revised the 2024 job statistics down by 911,000. “The economy should be in recovery mode,” Wong said. She identified five tailwinds for 2026: declining trade policy uncertainty, fiscal stimulus from tax legislation, easy financial conditions, AI-driven investment, and cyclical recovery. Wong estimated the Federal Reserve’s reaction function shifted dovishly. “It is as if their inflation target is no longer 2% but 2.8%,” she explained. The Fed projected core PCE inflation above its 2% mandate for eight years. Wong lowered her unemployment forecast from 5% to 4.4% due to immigration crackdowns and AI-related wealth effects.

Regarding Trump’s tariffs, Wong found that importers absorbed 95% of the costs. Only 30 cents of every tariff dollar passed through to consumer prices. “Almost 70% of the tariff costs are absorbed somewhere between the end point of the consumer prices and the import prices,” she said. Firms lacked pricing power during the contractionary shock but would gain leverage during recovery. Wong predicted more pass-through in 2026 as the economy strengthened. She identified credit markets as the primary risk. “Private credit is a very shadowy corner of the market,” she said, noting hidden balance sheet problems could trigger contagion if one firm failed.

Start Of Monetary Reset? What’s Next For Bitcoin, Gold, Dollar

Jim Thorne, Chief Market Strategist at Wellington-Altus Private Wealth, predicted Bitcoin would outperform gold over the next six months despite maintaining long-term bullish targets of $5,000 gold and $500,000 Bitcoin. He called for profit-taking on gold’s parabolic move. “I do not suggest you buy parabolic moves,” Thorne said. He expected gold to retrace to $3,700 before resuming its climb. Thorne credited Treasury Secretary Scott Bessent with averting a financial crisis through supply-side economics. The Trump administration’s plan to make 100% of capital expenditures tax-deductible through 2031 would trigger a spending supercycle. “We are going to have a capex super cycle,” he explained. The United States needed to increase electricity capacity by 90 to 100 gigawatts to support artificial intelligence. Thorne maintained his S&P 7,000 target and pushed back against narratives predicting the dollar’s demise.

On stablecoins, Thorne endorsed the Genius Act, which requires treasury backing for new issuances. The legislation would create demand for government debt. He noted the Federal Reserve held a symposium on crypto payments, signaling acceptance. Thorne discussed Canada’s economic problems. “Trudeau and Freeland’s economic policy for the last 10 years has been an absolute catastrophe,” he said. New Prime Minister Mark Carney needed to pivot toward natural resources and artificial intelligence. Gold represented 13% of the Toronto Stock Exchange, which Thorne considered excessive. He expected the Bank of Canada’s rate cuts to 1% by spring would boost Canadian real estate and banks.

Interest Rates To Zero, Rents Will Double; Grant Cardone On ‘Explosion’ In 2026

Grant Cardone, Founder and CEO of Cardone Capital, predicted interest rates would hit zero by June 2026 and mortgage rates would fall below 3.5%. He addressed regional bank troubles tied to commercial real estate debt. “There are trillions of dollars, about 3.7, maybe 3.8 trillion of debt that is hitting maturity right now,” he said. Cardone explained properties financed at 3% could not support values when rates hit 7%. He owns $5 billion in real estate with $240 million in adjustable debt facing similar pressure. Commercial real estate offered massive opportunities at 20% to 40% discounts to replacement costs. Residential properties remained insulated. “70% of single-family homes have a fixed-rate long-term loan below 4%,” he explained.

Cardone expressed concern about Bitcoin conference optimism in Vegas, where 35,000 attendees gathered. “These were the most optimistic people in the world, bro,” he said. He worried about AI and Bitcoin treasury companies being overhyped. Cardone advised investors to focus on one vertical rather than diversify. “Most of these people are very, very focused,” he said of the wealthy. He planned to launch a hybrid product combining real estate and Bitcoin. His 10X Wealth Conference in Miami would feature family office managers from billionaire families discussing tax strategies. “Getting rich is one thing,” he explained about concentration versus diversification.

Biggest Silver Squeeze Ever: Is $100 Next Or Collapse?

David Morgan, Publisher of The Morgan Report, discussed silver’s 11% decline from $54 to $48 following Trump’s tariff announcements and market volatility. Morgan explained the pullback was healthy after extended overbought conditions. “Markets fall faster than they go up,” he said. The $50 level represented a psychological barrier that held significance since 1980. Morgan noted the open interest remained steady despite the price drop. “The guys that are on what I would say the wrong side of this market that expect the price to keep coming down may not get their wish,” he explained. Shorts had difficulty covering positions. Morgan released a documentary titled Silver Sunrise, examining stress on the monetary system and precious metals.

Morgan warned of a potential natural squeeze driven by industrial demand. The semiconductor industry required 44 million ounces annually, and solar manufacturing needed hundreds of millions more. “The market itself says, I need silver or I’m going to die because I’m out of business unless I have it,” he said. The Silver Institute reported a 149 million-ounce deficit in 2024, with projections of 117 million ounces in 2025. Morgan calculated that only 600 million ounces remained in commercial inventory after subtracting retail holdings. The LBMA faced delivery issues that temporarily widened spreads. Retail investors who bought at $35 sold near $50, but new buyers emerged at higher levels.

What To Watch

*Data subject to delay if government shutdown continues

Wednesday, Oct 29

*Advanced U.S. trade balance in goods

*Advanced retail inventories

*Advanced wholesale inventories

Pending home sales

FOMC decision and press conference

Thursday, Oct 30

*Initial jobless claims

*GDP

Friday, Oct 31

*Personal income

*Consumer spending

*PCE index

*PCE (year-over-year)

*Core PCE index

*Core PCE (year-over-year)

*Employment cost index

Chicago Business Barometer (PMI)

Fascinating compilation of market analysis. The Costco references in both Shapiro's and Tiggre's interviews are particularly telling - when retail buyers are asking about silver at Costco and products are selling out there, it's a clear sign of main street participation. Costco has become an unexpected barometer for precious metals sentiment because their customer base represents the 'smart retail' segment - people who comparison shop and research before buying. The fact that silver sold out at Costco while the price went from $35 to $50+ shows genuine physical demand, not just paper speculation. However, as both guests noted, this kind of enthusiasum from casual investors is exactly what tends to mark market tops. The contrarian play might be to watch when Costco stops restocking silver - that would signal the retail mania has truly peaked.