Fed’s 50 Bps Rate Cut: Will It Trigger Inflation AND A Hard Landing?

Here's What's Next After The First Rate Cut Since 2020

TABLE OF CONTENTS

ECONOMY: The Fed is “too late” with rate cuts, said Anna Wong

TECH: Bradley Tusk on how the Fed could affect the tech sector

SILVER: Silver will outperform gold according to David Morgan

MARKET RECAP

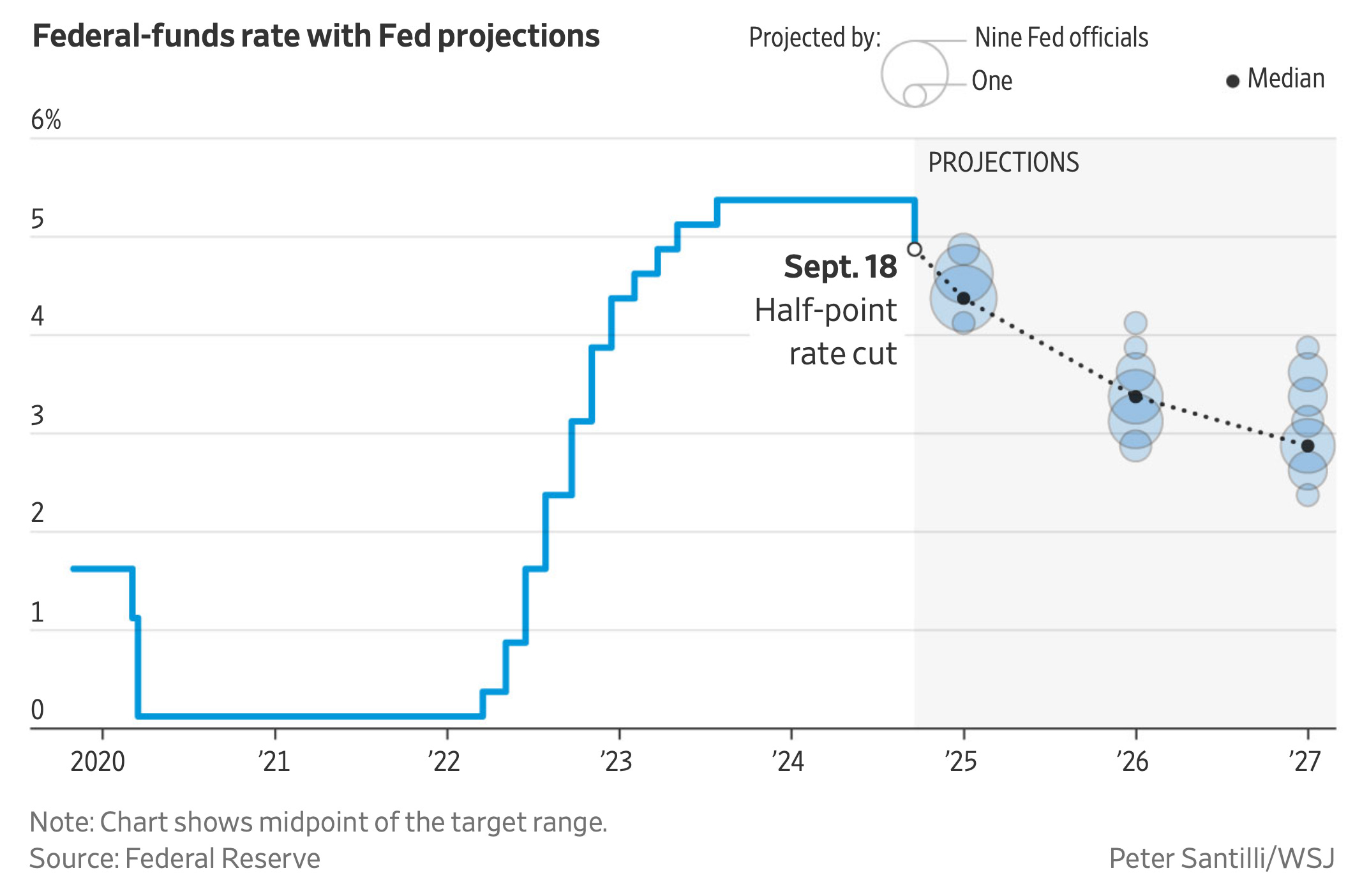

Latest News. The Federal Reserve cut interest rates by 50 bps on Wednesday. This is the first cut in four years, and puts the Federal Funds Rate in the target range of 4.75 to 5 percent. The Fed also said that it intended to reduce rates by a full percentage point by year-end.

“This recalibration of our policy stance will help maintain the strength of the economy and the labor market,” said Fed Chairman Jerome Powell, at a press conference following the rate cut announcement. “We also decided to continue to reduce our securities holdings.”

Stocks fell immediately following the announcement, with the S&P down 0.3 percent and the Dow Jones down 0.25 percent. The yield on the 2-year note, which is sensitive to monetary policy changes, fell by 0.06 percentage points to 3.6 percent.

Powell added that “there’s nothing in (the Summary of Economic Projections) that suggests that the committee is in a rush to get this done,” emphasizing the Fed’s cautious approach to rate cuts.

To make sense of these market data and Fed policy, we were joined by Steve Hanke, Professor of Applied Economics at Johns Hopkins University, and a frequent guest on the show.

Hanke said that the Fed’s interest rate cut misses the bigger picture, which is the money supply, as measured by M2.

“All this fuss about interest rates is kind of a tempest in a teacup,” said Hanke. “It’s really a second or third-order condition. The first-order condition is what’s going on with the money supply.”

He said that the money supply, measured by M2, has been contracting since July 2022, and historically, such contractions have led to recessions. According to Hanke, this contraction suggests that a recession lies ahead, and could already in fact have arrived.

The professor downplayed the recent increase in M2 growth, calling it insignificant. He said that the current M2 growth rate of 1.26 percent is still far below his “golden growth rate” of 6 percent, which he considers necessary to achieve the Fed’s 2% inflation target.

The conversation then turned to a letter that three Democratic senators wrote to Powell on Monday, September 16th, requesting a 75 bps rate cut. The letter read, “The [Federal Open Market] Committee must consider implementing rate cuts more aggressively upfront to mitigate potential risks to the labor market.”

Hanke described the letter as politically motivated, aiming to pre-emptively blame the Fed for any economic downturn while distancing the senators themselves from the repercussions of a recession. He also said that the senators had failed to understand monetary policy properly.

“The letter from the senators shows that the staff who wrote it doesn’t understand what’s going on,” Hanke remarked. “They’re just focusing on the interest rate. They never talked about the Fed’s balance sheet or the money supply contracting.”

Market Movements

From September 11 to September 18, the following assets experienced dramatic swings in price. Data are up-to-date as of September 11 at 4pm ET (approximate).

Redfin Corporation — up 27.5 percent.

Sirius XM Holdings — down 17.7 percent.

Coffee — up 6.9 percent.

Aluminum — up 7.8 percent.

WTI Crude Oil — up 6.5 percent.

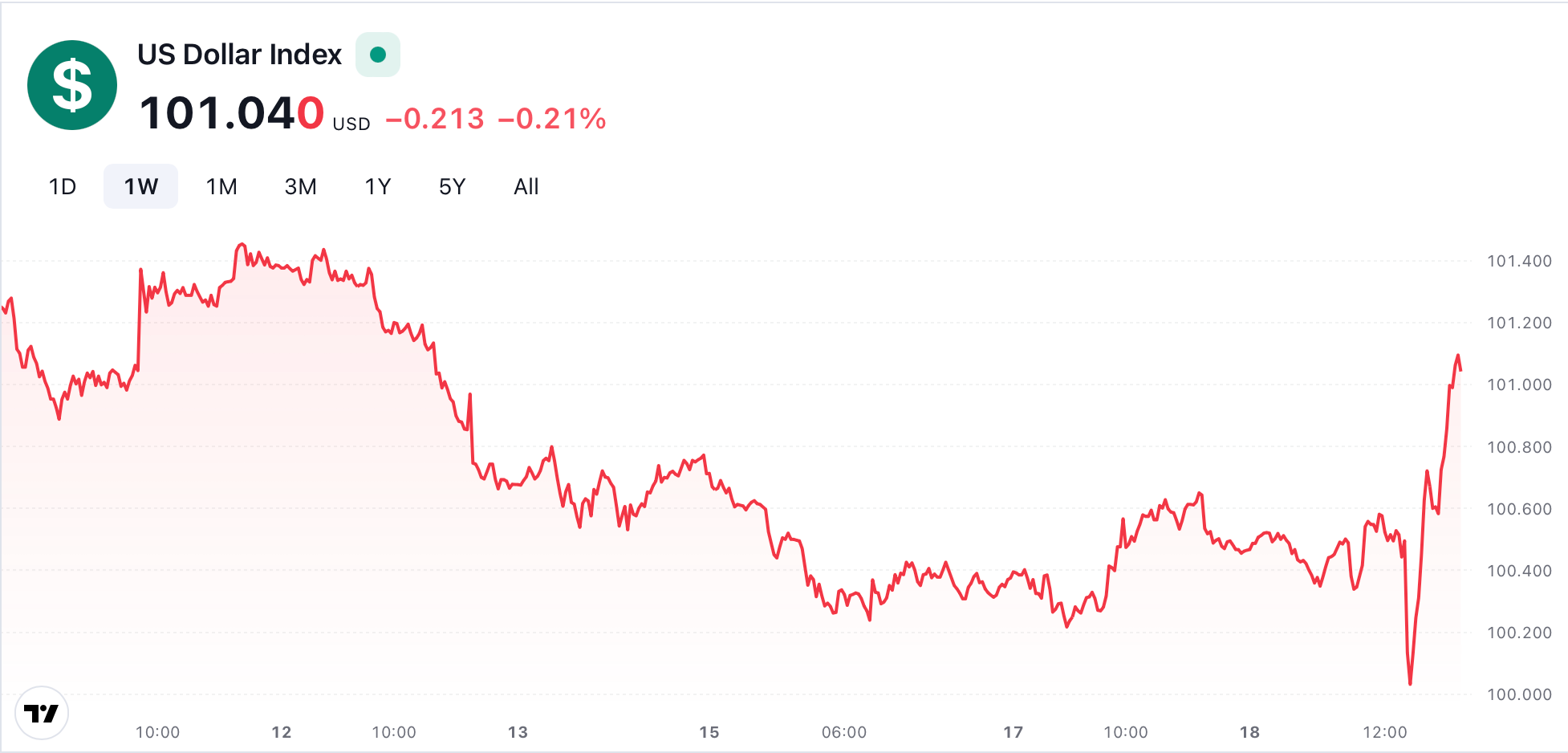

DXY — down 0.21 percent.

Bitcoin — up 7.6 percent.

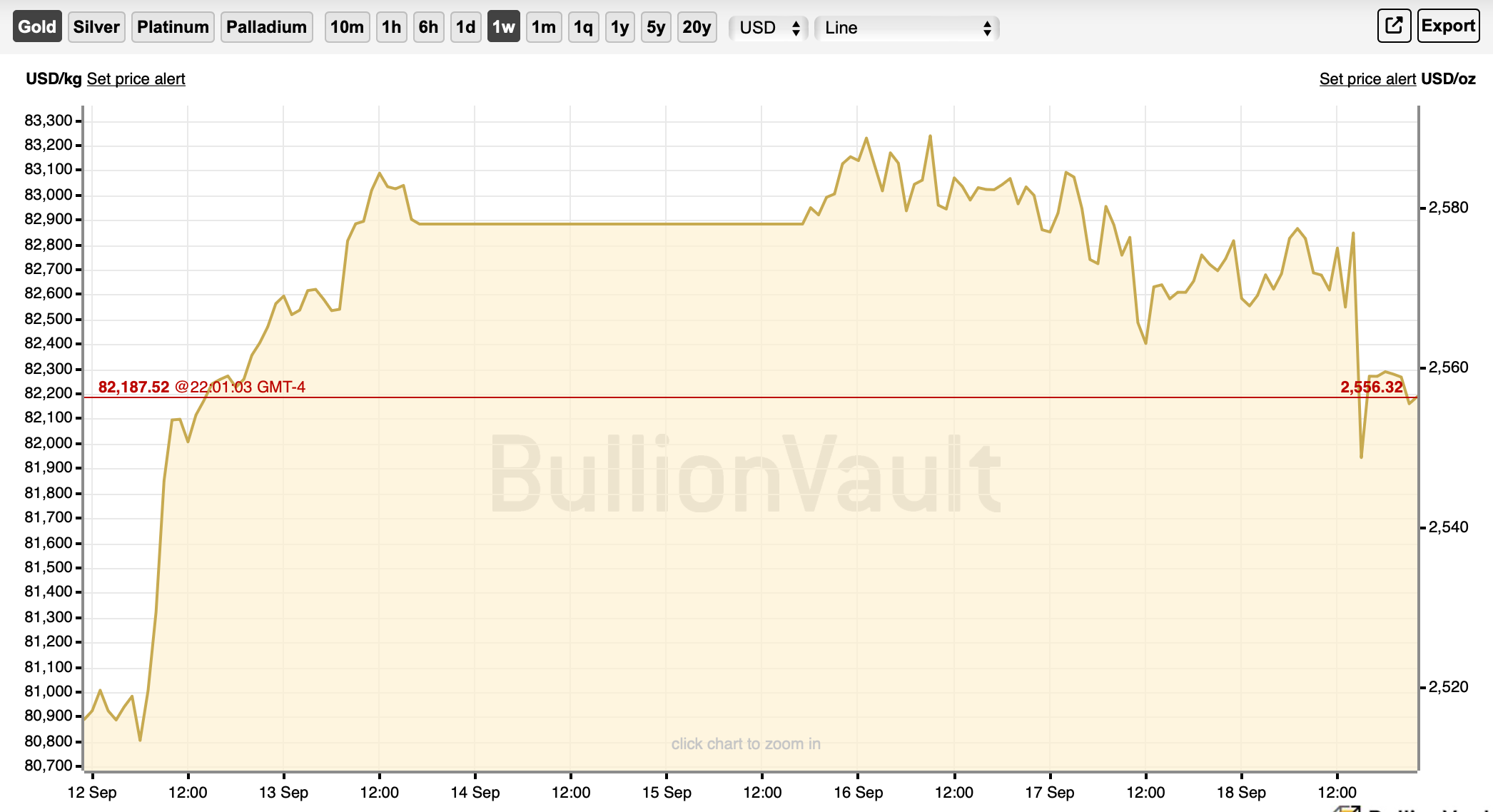

Gold — up 1.8 percent.

10-year Treasury yield — up 2.3 percent.

S&P 500 — up 1.2 percent.

Russell 2000 — up 4.9 percent.

USD/Yen — up 0.8 percent.

ECONOMY:

FED IS ‘TOO LATE’ TO STOP ‘STEEPENING’ RECESSION

Anna Wong, September 13, 2024

Anna Wong, Chief U.S. Economist for Bloomberg Economics, said that the Federal Reserve (Fed) would be too late in cutting interest rates, potentially deepening a recession.

“The Fed is waiting for layoffs to happen before they want to cut rates,” said Wong. “It’s already too late. In all previous recessions, layoffs typically happen well into recession.”

Wong said that the Fed had been waiting for clearer signs of economic distress, such as higher unemployment or widespread layoffs, before considering rate cuts. However, by the time these indicators became evident, recessionary forces would be inevitable.

Wong said that the labor market was already showing signs of weakness, as evidenced by slowing job growth and increasing layoffs. The unemployment rate, which was rising for four consecutive months, surprised many forecasters. Wong claimed that unemployment would continue to rise.

“We have been of the view that the unemployment rate will rise to 4.5 percent by the end of this year,” said Wong. “Next year, it will continue to climb until hitting 5 percent, and stabilize thereafter, and falling form 5 percent only in 2026.”

The unemployment rate currently sits at 4.2 percent.

She dismissed claims that rising unemployment was solely due to immigration, explaining that layoffs were already playing a significant role in the increase. Additionally, she noted that layoffs were accelerating in sectors like construction and healthcare, contrary to the usual seasonal trends.

Wong highlighted the recent downward revisions in non-farm payroll data, suggesting that the labor market was weaker than initially reported. According to her analysis, job growth had turned negative months earlier, a signal of underlying economic contraction.

She further pointed out that household savings rates were falling to levels reminiscent of the 2008 financial crisis, indicating that consumers might struggle to sustain spending in the face of higher unemployment.

DEMOGRAPHY:

’VIOLENT’ AND ‘EXPLOSIVE’ FOURTH TURNING IS HERE

Neil Howe, September 17, 2024

The U.S. is at high risk of facing either a civil war or a global conflict according to Neil Howe, Head of Demography at Hedgeye and Co-author of The Fourth Turning: An American Prophecy — What the Cycles of History Tell Us About America’s Next Rendezvous With Destiny.

Howe said that, as per his research, major crises occur every 80-100 years, and that these “fourth turnings” often involve war or civil conflict.

“Fourth Turnings are by their very nature violent, explosive, and unpredictable, but they lead to great change; they lead to huge structural change,” remarked Howe.

Howe said that the current global situation, marked by growing pessimism and populism, fits the pattern of a Fourth Turning. He pointed to the increasing polarization and populism in politics as evidence that societies are approaching a generational crisis. He also mentioned specific events — the 2008 financial crisis, the 2020 pandemic, and the 2022 Russian invasion of Ukraine — as manifestations of “The Fourth Turning.”

Howe also mentioned that inflation is a tool used during these periods to distribute economic burdens, stating that it is not a bug but a feature of such crises. Historically, Fourth Turnings have involved significant conflicts and economic adjustments, and Howe suggested that today's political and economic environment shows similar signs of stress and transformation.

Because Howe expected inflation to re-emerge, he suggested that assets which protect against inflation would be the best investments. In particular, he cautioned that long-term bonds are vulnerable to erosion from inflation, while inflation-protected bonds, commodities, precious metals, private equity, and real estate could see increases in value.

TECH:

WHAT FED PIVOT WILL DO FOR TECH STOCKS

Bradley Tusk, September 15, 2024

Bradley Tusk, Founder and CEO of Tusk Ventures, joined the show to discuss how the Fed rate cut could impact the tech sector.

He explained that a Federal Reserve rate cut would significantly impact tech by increasing liquidity and lowering capital costs. This, he argued, would be especially beneficial for the venture world, where a liquidity crunch has stifled IPOs and mergers. However, he warned that over-reliance on a few tech giants, such as Nvidia, is risky, particularly when market valuations are based on optimistic assumptions about AI's future profitability.

“You have to truly believe that consumer spend on AI products is going to be really meaningful, otherwise demand...is going to fall,” said Tusk. “Ultimately, unit economics matter, profitability matters, margin matters. You can’t just acquire growth at all costs.”

Tusk highlighted several problematic trends in early-stage tech investment, noting that many companies had fallen for “gimmicks” like VR, Web 3, and NFTs, which he described as “a joke.” He stressed that “you can’t run an investment fund just based on narrative; you’ve got to run it based on results and returns.”

Regarding investment trends, Tusk indicated a shift towards sectors like AI, data privacy, electrification, and defense technology. He emphasized the importance of focusing on areas with clear regulatory paths and practical applications, rather than speculative technologies. He cited FanDuel and Lemonade as successful examples of startups that identified unmet consumer needs and executed effectively.

GOLD:

HOW GOLD COULD REACH $2,700 BY YEAR-END

Gary Wagner, September 16, 2024

Gold reached an all-time high of almost $2,600 per ounce this week, and to discuss what is next for the yellow metal, we were joined by Gary Wagner, Editor of TheGoldForecast.com.

Given the likelihood of multiple Fed rate cuts, Wagner reiterated his belief that gold would reach $2,700 an ounce by year-end or early next year. He acknowledged the possibility of gold exceeding this target, stating, “I would like to be wrong in that way. I would like to see gold go higher than my target.”

This optimism was tempered by his caution that any unexpected decisions by the Fed, such as pausing rate cuts, or failing to follow through with additional cuts, could create bearish tailwinds for gold.

Wagner also said that gold could reach $3,000 an ounce, but that this would be driven by further economic or geopolitical uncertainties, and it would likely happen over a longer timeframe, possibly extending into the first quarter of next year. Wagner mentioned that he would “like to be wrong” about his conservative estimate if gold outperforms his expectations and reaches $3,000 sooner.

Furthermore, Wagner pointed out that central banks' strong demand for gold, as they add to their reserves, is another supportive factor for gold prices. He mentioned that this demand, coupled with the overall market sentiment anticipating lower interest rates, creates a favorable environment for gold to reach his target of $2,700 an ounce by the end of the year.

SILVER:

SILVER TO OUTPERFORM GOLD AS NEW MONETARY SYSTEM EMERGES

David Morgan, September 14, 2024

David Morgan, Publisher of The Morgan Report, joined the show to discuss his thesis that the global monetary system would radically transform over the next three years, benefitting silver.

Morgan said that moves away from the U.S. dollar and increased attention in alternative currencies like those proposed by BRICS nations, could raise demand for silver. Precious metals in general would benefit as the U.S. dollar loses its appeal. He predicted that nationalistic economic policies might result in countries hoarding silver as a strategic resource, further tightening supply.

Morgan pointed out that over 70 percent of silver's demand comes from industrial use, with only a small fraction attributed to investment demand. However, he believes that this dynamic could shift dramatically. If economic conditions worsen and gold prices rise significantly, a surge in investment demand for silver could push its price to outperform gold by a ratio of “two to one, three to one, or even four to one.”

He argued that gold currently serves as a barometer, indicating economic distress and instability. Morgan noted that while higher gold prices signal “stormy times ahead,” many people may turn to silver as a more affordable investment alternative. As gold prices rise and become unaffordable, he anticipates a spillover effect where investors shift towards silver.

“I can't afford a gold coin at $3,200 an ounce, but I can still buy silver at $70,” said Morgan.

WHAT TO WATCH

Thursday, September 19, 2024

Bank of England interest rate decision: The Bank of England’s monetary policy committee will decide on the direction of interest rates.

Bank of Japan interest rate decision: The Bank of Japan’s monetary policy committee will meet to decide on the direction of its key interest rate.

People’s Bank of China interest rate decision: The Peoples’ Bank of China will set its policy interest rate.

Initial Jobless Claims: This measures how many American workers applied for unemployment insurance for the first time during the past week.

Existing Home Sales: This shows the number of sales of existing homes, and is released monthly by the National Association of Realtors (NAR).

Tuesday, September 24, 2024

S&P Case-Shiller Home Price Index (20 cities): This measures the changes in residential home prices in 20 major metropolitan areas across the United States.

Wednesday, September 25, 2024

New Home Sales: This measures the number of newly constructed single-family homes sold.

Thursday, September 26, 2024

Initial Jobless Claims: This measures how many American workers applied for unemployment insurance for the first time during the past week.

Pending Home Sales: This measures the number of homes under contract but not yet closed, indicating future activity in the housing market.

Friday, September 27, 2024

Personal Consumption Expenditures: This measures the average level of prices paid by consumers for goods and services and is the Federal Reserve's preferred gauge for inflation.